(855) 935-4671

(855) 935-4671

Sarasota Insurance Agency >> blog

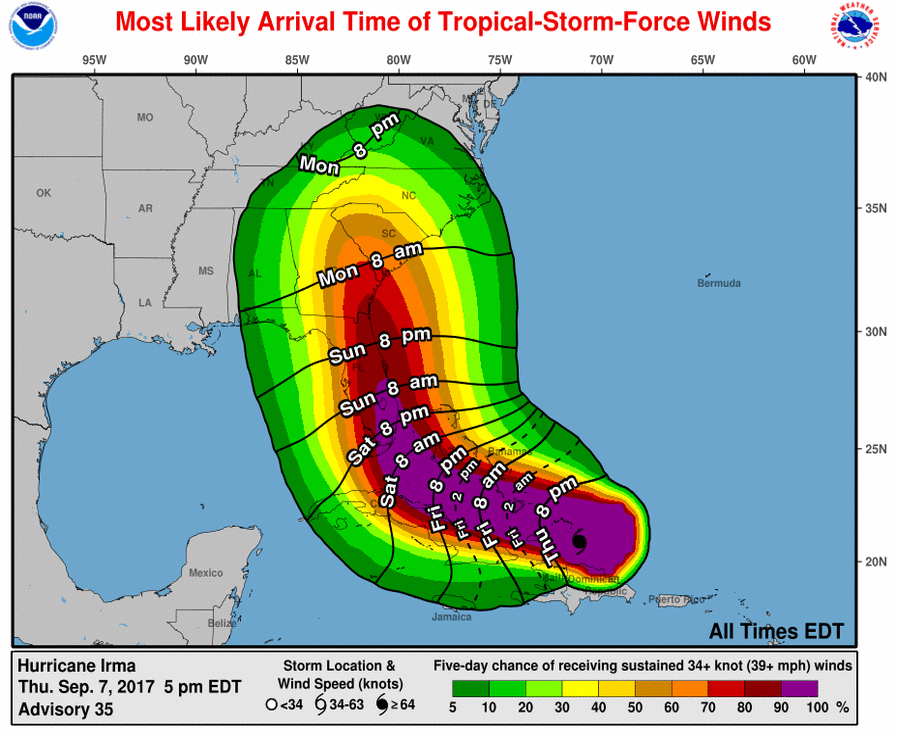

With long to-do lists, right now most of us are working hard to get ourselves, our families and our homes prepared for Hurricane Irma.

Personal safety comes first, of course. But as we firm up plans to stay out of harm’s way, state insurance officials and Florida’s top insurance companies are urging everyone in Irma’s path to plan ahead to avoid complications if we have to file damage claims after the storm.

“Hurricane Irma is a large and dangerous storm, capable of creating widespread damage, and it is crucial for consumers to understand their insurance coverage as they prepare their homes for Irma’s possible impact,” Florida Chief Financial Officer Jimmy Patronis said Thursday.

The CFO’s office urged residents to include copies of their insurance policies in their disaster kits and to call the state’s insurance help line [877-693-5236] with any insurance-related questions or concerns.

Here are some insurance tips to help you both before and after the storm.

Read your property and flood policies carefully and ask questions long before a storm approaches. Does it cover wind damage? Check coverage for Additional Living Expenses. This covers hotel bills, restaurant meals and other expenses if your home is rendered uninhabitable.

Protect your home or property by covering windows with hurricane shutters or plywood to guard against flying objects, move vehicles into garages or carports, carry in grills and outdoor furniture to prevent them from becoming flying objects. If you live in a low-lying area, utilize sandbags and plastic sheeting to protect against rising water.

Make records of your home and possessions. Compile an inventory with estimated values and send it to the cloud for easy retrieval later. Do the same with a still or video camera. One easy way is to walk through your home and record video with your smartphone. Narrate what is being recorded and include value or replacement costs. Then upload your video to the cloud. This will help establish your claim.

Follow your insurance company on social media for important storm-related information. Save your insurance company’s or agent’s phone number for ease of filing future claims.

Review the “Duties After Loss” section of your policy. Failure to follow the provisions in this section could result in non-payment on your legitimate claim.

Make sure your insurers have up-to-date contact and mortgage company information.

Have copies of your insurance policies in a safe waterproof and easy to access location, along with other important documents such as deeds, wills, health records, financial records, pet records, identification details, home inventory, etc. Photograph or scan your documents and save them to the cloud for easy retrieval in the event of a loss.

Call your insurance agent immediately. Most major insurers have toll-free phone numbers.

Take pictures/video of damaged property. Keep notes and use inventory lists to help adjusters assess damages.

Be aware of your hurricane deductible ranging from 2 percent to 10 percent of your home’s insured value. For some policies, a $500 flat deductible applies. Whatever your deductible, you will be responsible for it.

Secure replacement costs/estimates from local retailers, and obtain statements from vendors on items that cannot be repaired.

Begin making temporary repairs to prevent further damage. Save all receipts. But don’t make permanent repairs until an insurance adjuster has inspected it.

Do not dispose of damaged contents until authorized by your agent or claim representative.

Insurers usually don't pay for removal of trees or debris that blew into your yard without damaging an insured structure.

Let your insurer know how to reach you if your home is uninhabitable or you move somewhere else temporarily.

Be careful about signing anything from contractors before speaking with your insurance company. Some contractors might try to persuade you to sign document called an Assignment of Benefits which transfers rights to seek payment for your claim, including filing lawsuits.

Don't assume that adjusters will know what street they are on; street signs may have blown away. Industry officials say spray-painting important information on homes after a hurricane has proven effective. But don't include your policy number; someone else may take advantage of that.

Be patient. Insurers usually send adjusters to the worst-hit homes first.

Many adjusters and agents are authorized to issue checks on the spot to cover the cost of temporary housing.

If confused about your claim or dissatisfied with your insurance adjuster’s findings, consider seeking help from a public adjuster. A list of licensed adjusters is available from the Florida Association of Public Insurance Adjusters at www.fapia.net.

Claims hotlines for top insurers in South Florida:

American Bankers Insurance Co.: 888-260-7736

American Traditions Insurance Co.: 866-270-8430

Anchor Insurance: 844-365-5588

Capitol Preferred Insurance Co.: 888-388-2742

Castle Key Insurance (Allstate): 800-255-7828

Citizens Property Insurance Corp.: 866-411-2742

Edison Insurance Co.: 888-683-7971

Federated National Insurance Company: 800-293-2532

Florida Family Insurance Co.: 888-486-4663

Florida Peninsula Insurance Co.: 866-549-9672

Frontline Insurance: 866-673-0623

Heritage Property & Casualty Insurance: 855-415-7120

Homeowners Choice Property & Casualty Insurance Co.: 866-324-3138

Modern USA Insurance Co.: 866-270-8430

People’s Trust Insurance Co.: 877-333-1230

SafePoint Insurance Co.: 855-252-4615

Southern Fidelity Insurance Co.: 866-874-7342

Southern Oak Insurance Co.: 877-900-2280

St. Johns Insurance Co.: 877-748-2059

Tower Hill Insurance: 800-342-3407

United Property & Casualty: 888-256-3378

Universal Property & Casualty Co.

Universal North America: 866-999-0898

rhurtibise@sun-sentinel.com, 954-356-4071, twitter: twitter.com/ronhurtibise

2017-09-08 10:09:51

Our goal is to offer money saving solutions that provide our clients with a cost effective and comprehensive insurance package.

Copyrights © by West Florida Insurance Agency, Inc 2017